![[Power book cover]](https://richardheinberg.com/wp-content/uploads/2021/03/cover_POWERcatalog-proof_300x450.jpg)

MuseLetter #296 / January 2017 by Richard Heinberg

Download printable PDF version here (PDF, 430KB)

This month marks 25 years of MuseLetter. During this time I’ve written and published something like 1,200,000 words, which found their way into a dozen books. Special greetings to long-time subscribers—you know who you are—who remember the printed version of this publication (1992-2007), which went out monthly with the help of two or three immensely helpful volunteers. Currently I have no new book project in mind, but plan instead to produce shorter or longer pieces like the ones in this month’s issue, in response to events and developments in energy, politics, and the ecosphere. Have a safe and happy new year!

The frequency of Internet searches for the term “peak oil” has waned dramatically in recent years; now even the number of articles announcing the “death” of peak oil has dwindled, so universal is the assumption that the concept is completely debunked. Why bother beating a dead horse? With supreme irony, it could be within the next few years when the maximum-ever rate of world oil production is actually achieved, to be followed by terminal decline. It’s too early to make a definitive claim, but the evidence is starting to stack up. And the implications are mind-boggling.

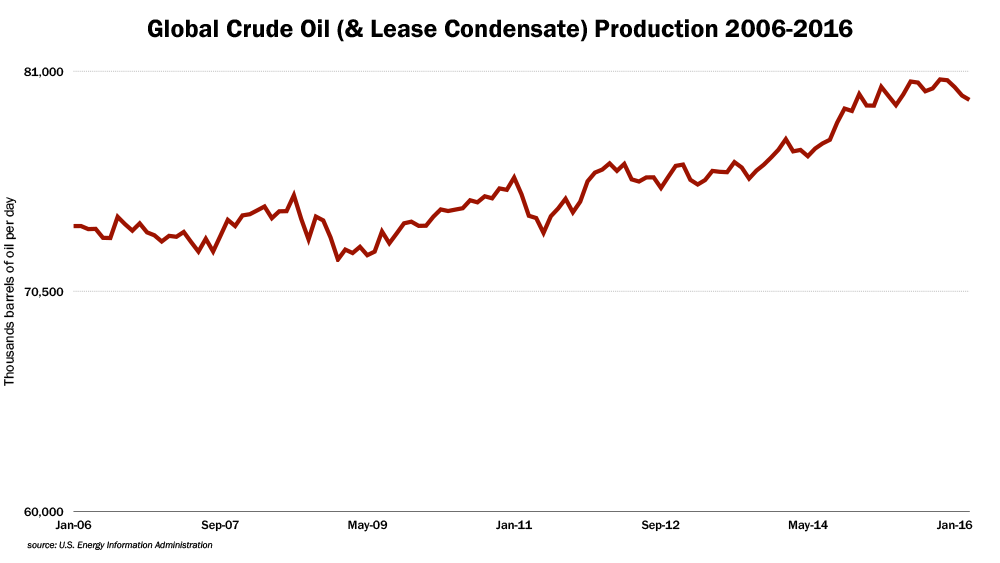

Last year’s average daily oil production rate will probably end up (when authoritative statistics are published) being about the same as 2015’s—roughly 80 million barrels per day, if we count crude oil only and exclude biofuels and natural gas liquids. And 2017’s output may well be down, due to the industry’s cutbacks on investment in new projects.

Figure 1. Global Crude Oil (and Lease Condensate) Production, 2006-2016. Source: U.S. Energy Information Administration

Yet there are good reasons to be cautious in claiming a peak. Famously, several analysts have already called the peak too early—in 2005, 2008, and 2010. It was an understandable error. World production of conventional oil was indeed stalling during that time; what the too-early peakists missed was that a combination of extremely high oil prices, loose regulation, and stupid-easy financing would lead to increasing rates of extraction of marginal resources like tar sands and tight oil, starting in 2011. Further, the precise date of the global peak actually has relatively little significance, as the economic impacts of oil depletion will be spread over many years before and after that date. Indeed, those impacts have been visible for at least the past decade and arguably much longer, taking the forms of booming and crashing oil prices; economic turmoil within the oil industry; flattening demand, particularly in highly developed nations; and military conflicts in the Middle East. Nevertheless, the term “peak oil” implies a point in time, and plenty of people will disregard the very notion of a peak until it can be demonstrated in the rear-view mirror of oil production statistics.

In the 2003 edition of my book The Party’s Over, I endorsed the forecast of petroleum geologist Jean Laherrère for a peak of conventional world oil production in 2010, and of unconventional oil (and therefore total world oil) in 2015. Current statistics suggest that Laherrère probably made the best of the various peak-oil forecasts. Laherrère has continued to update his analysis in the intervening years, and on the basis of current data believes world oil production is peaking essentially now.

There was a lot that just about all peakists got wrong. Most of us subscribed to a simplistic notion of energy economics in which, as depletion bit harder, oil prices would just go up and up (I made no attempt to forecast oil prices in The Party’s Over). Well, prices did shoot higher for a while, and that’s when the peak oil concept gained its widest exposure. But high prices killed demand and also incentivized much higher rates of production of very-high-cost oil. The eventual result was the situation we see now, where tepid demand confronts a supply glut resulting from drillers spending other people’s speculative money on unprofitable tight oil projects—and an industry therefore operating in crisis mode. Recently, we’ve seen more sophisticated energy-economy analysis from Gail Tverberg and others, explaining why petroleum depletion can result in low oil prices and a temporary supply glut, as consumers’ ability to afford oil declines faster than actual oil production does.

Any talk of peak oil today faces seemingly contradictory evidence. OPEC has recently cut back on supplies in order to reduce a global glut of crude, and oil prices are down significantly from levels seen in the years 2011-2014. Also, enormous amounts of oil sit in storage. Surely (the conventional wisdom goes) as soon as the market rebalances, oil prices will go back up, drilling and exploration will resume again, and production rates will hit new record levels. For reasons we’re about to explore, that conventional wisdom may be as flawed as peakists’ early understanding of oil economics.

I will present two exhibits on which to base my case for that assertion. I’ll also offer a quick review of a couple of new and relevant books. Then, in a fairly long final section, I’ll discuss the implications of a possible peak of world oil production in today’s economic and political context. This will entail an exploration of whether Donald Trump might turn out to be the peak oil president, and what that may mean in terms of policies and outcomes. This is a lot of ground to cover; indeed, I thought about dividing this essay into several smaller posts. However, the themes seemed just too deeply intertwined. In any case, the result is fairly lengthy and meandering, so have a cup of tea handy.

Exhibit A: David Hughes’s Reports, Including “2016 Tight Oil Reality Check”

During the past dozen years world conventional oil production has flatlined, as noted above, and nearly all of the increase in global supplies since 2005 has come from unconventional sources—tar sands, tight oil in the U.S. (produced through hydrofracturing and horizontal drilling), and deepwater oil. It is U.S. tight oil that has done the most to boost global oil supplies in these years. Thus the prospects for future production from this resource are highly relevant for understanding the overall status of world petroleum.

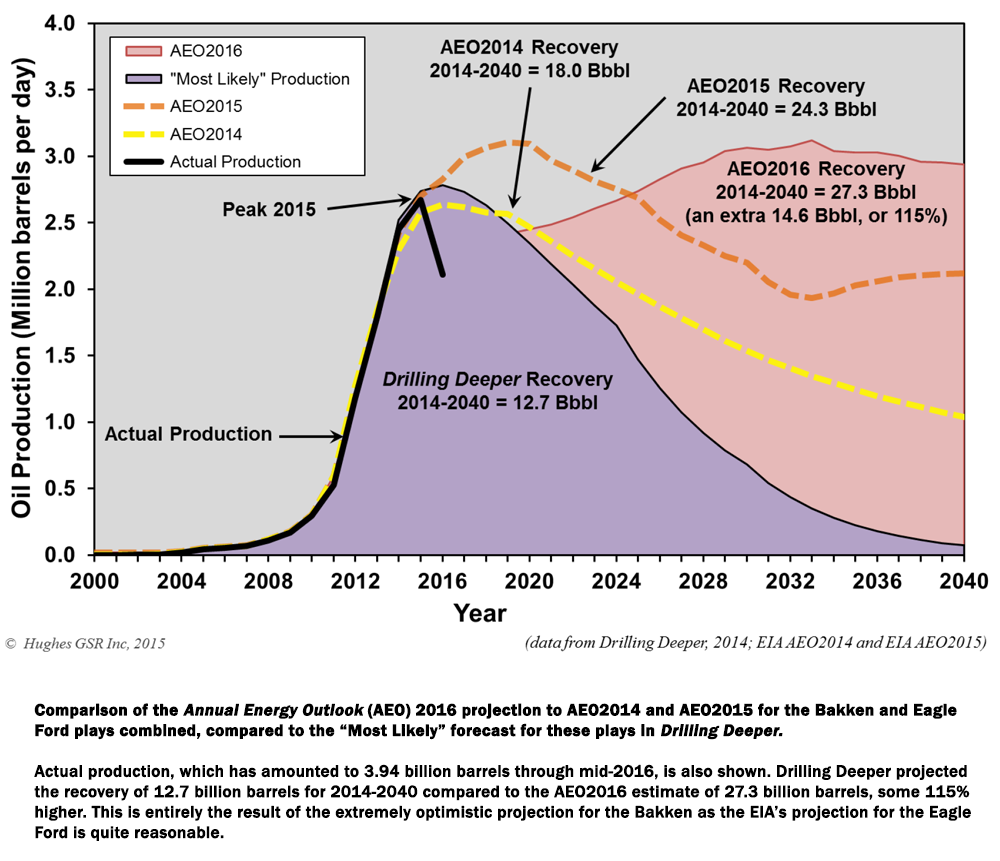

Figure 2. Comparison of the Annual Energy Outlook 2016 (AEO2016) projection to AEO2014 and AEO2015 for the Bakken and Eagle Ford tight oil plays combined, compared to the “Most Likely” forecast for these plays in Drilling Deeper. Source: J. David Hughes, 2016 Tight Oil Reality Check.

The oil industry and the Energy Information Administration (EIA) of the U.S. Department of Energy claim that tight oil production can expand at relatively low prices until roughly 2040, presumably forestalling world oil supply problems. However, the EIA’s forecast has drawn criticism. Since 2013, earth scientist David Hughes has been providing Post Carbon Institute with regularly updated, detailed assessments of American shale gas and tight oil resources and production. His first publication in the series, Drill, Baby, Drill, made two important points:

“First, shale gas and shale oil wells have proven to deplete quickly, the best fields have already been tapped, and no major new field discoveries are expected; thus with average per-well productivity declining and ever-more wells (and fields) required simply to maintain production, an ‘exploration treadmill’ limits the long-term potential of shale resources. Second, although tar sands, deepwater oil, oil shales, coalbed methane, and other non-conventional fossil fuel resources exist in vast deposits, their exploitation . . . require[s] . . . enormous expenditures of resources and logistical effort. . . .”

Hughes’s latest report examines the EIA’s most recent forecasts for tight oil. Since the oil price collapse of mid-2014, costs of production have declined and well productivity has increased. These developments have led many observers (including the EIA) to assume that the industry is learning, technology is improving, and tight oil production (which has fallen by nearly 20 percent since early 2015) will soon rebound to new highs. But Hughes points out that improvements in per-well productivity are mostly due to “high-grading”—the practice of curtailing drilling outside relatively small “sweet spots” where resources are concentrated. The length of horizontal wells has increased,

“. . . but as each well can now drain more of the reservoir it has reduced the number of locations available to drill. The net effect is that, at a constant drilling rate, better technology will exhaust a play more quickly at a lower cost—but will not substantially increase ultimate recovery.”

As for declining production costs, Hughes is skeptical that this is a sustainable trend:

“The improvement in the number of wells a rig can drill per unit of time has partially offset the effect on production of the steep decline in rig counts since mid-2014, and has improved economics. The service industry’s rate cuts have also had a major impact on the economics of the average well. But there are a limited number of drilling locations in sweet spots, and high grading plus the downturn in oil prices has resulted in their exhaustion at disproportionately high rates, leaving higher-cost oil for later. An analysis of top counties in plays like the Bakken and Eagle Ford shows that average well productivity has begun to decline, meaning that the best locations have been exhausted along with possible well interference (from wells being drilled too close together).”

If oil prices tick much higher, service companies will hike their rates again. Overall, tight oil producers have been losing money for years, and that situation doesn’t look likely to change.

Hughes assigns a “very high” optimism bias rating for the overall EIA 2016 tight oil forecast, “based on the fundamentals, given what is known from an analysis of well quality and production data from subareas within each play.” His reports suggest that even if oil prices had remained above $100 per barrel (instead of dropping in 2014 to its current range of $35-$60), U.S. tight oil production still would have ended up peaking before 2020. If oil prices significantly rebound and drilling rates do the same, production will increase above current levels (already there has been a slight uptick in Bakken output); but even in that case, the glory days of U.S. tight oil are in the past. The high-water mark of production in early 2015 is unlikely to be surpassed by much, or for long, before terminal decline sets in.

Exhibit B: HSBC Report, “Global Oil Supply”

As noted above, conventional oil production rates have been on a plateau for over 10 years. A plateau cannot be considered a peak until overall production commences a sustained decline. Further, this plateau has provided a base from which unconventional oil (mostly tight oil) has boosted total world output to record levels. Therefore two questions central to any discussion of the direction of world oil production are:

- When will the plateau in conventional oil production end?, and,

- Will it terminate in a sustained production increase, or a decrease?

A recent report from the investment bank HSBC offers plenty of reasons for thinking the end of the plateau will come soon and long-term production decline will commence. Released in mid-2016 to little fanfare, the report Global oil supply: Will mature field declines drive the next supply crunch? does not address the topic of “peak oil” per se. Instead, it examines the rate at which production from currently producing oilfields is diminishing, and prospects for replacement of that production from new oilfields and with more intensive methods of production.

The authors calculate that 81 percent of current world oil production is from oilfields seeing declining rates of production. In their view, a “sensible range for average decline rate on post-peak production is 5 to 7 percent,” which equates to about 3 to 4.5 million barrels per day (mbd) of reduced production each year. “By 2040, this means the world could need to replace over 4 times the current crude oil output of Saudi Arabia (or more than 40 mbd), just to keep output flat.”

The authors also note that output from smaller oilfields typically declines twice as fast as that from large ones, and that “the global supply mix relies increasingly on small fields: the typical new oilfield size has fallen from 500-1,000mb [million barrels] 40 years ago to only 75mb this decade.” Further, new discoveries of oil are shrinking, partly due to shrinking exploration budgets—though the trend began long before the oil industry’s recent troubles. “Last year the exploration success rate hit a record low of 5 percent, and the average discovery size was 24mbbls [million barrels].”

All of this implies that, while in the past decade downturns in output from old oilfields were replaced with new production enabling steady overall conventional oil supplies, replacement of production is much more doubtful in the immediate years ahead.

“The oil market may be oversupplied at present, but we see it returning to balance in 2017. By that stage, effective spare capacity could shrink to just 1 percent of global supply/demand of 96mbd [of all liquid fuels including biofuels], leaving the market far more susceptible to disruptions than has been the case in recent years. Oil demand is still growing by ~1mbd every year, and no central scenarios that we recently assessed see oil demand peaking before 2040.”

HSBC evidently did not include “central scenarios” in which demand is curtailed by the implementation of climate change mitigation policies or as a result of general economic contraction. In a contraction scenario, which I regard as quite likely, it might be difficult to determine whether, and to what degree, economic decline resulted from the oil industry’s failure to maintain net energy productivity in the face of rising energy costs for its activities.

Bonus Exhibit: Reviews of Cold War Energy by Douglas B. Reynolds; and Failing States, Collapsing Systems by Nafeez M. Ahmed

Peak oil books have largely fallen out of fashion. For a few years, it seemed a new one was appearing every month; now the pace is down to about one or two per year. The most recent is by Douglas Reynolds, professor of energy economics at the University of Alaska, Fairbanks, and it’s a good one.

In his first chapter, Reynolds explains why peak oil killed the Soviet Union. Most historians attribute the USSR’s crackup—“one of the most significant economic events of the 20th century” —to economic mismanagement or an arms buildup by the Reagan administration, but Reynolds finds these explanations lacking. The more likely trigger, in his view, was a sudden decline in Soviet oil production. An initial peak in 1983 led to further investment and subsequent output stabilization. But in 1989 production fell again, then plummeted in 1990—falling about 25 percent in the years immediately after 1988. The mostly closed Soviet economy was not excessively dependent on oil export revenues; however, it did depend on oil as the primary energy source to run the nation’s transport and food systems.

Some observers claim it was the drop in world oil prices in the 1980s, orchestrated by the U.S. and Saudi Arabia, that killed the Soviet economy. Reynolds disputes this. He argues instead that Soviet oil production technology of the era had hit its limits, and it was scarcity of the physical commodity that undermined the nation’s economy and hence its political regime. Later, in the post-Soviet era, new enhanced oil recovery (EOR) technology, mostly imported from the U.S., enabled Russian oil production to achieve new record levels. EOR production will eventually hit its own limits, according to the author, though Russian output has so far (as of 2016) managed to avert a crash.

Reynolds applies this historical analysis to economic growth theory, arguing that conventional theory fails to take adequate account of the role of energy, particularly petroleum, in explaining the factors of growth. Further chapters address “Energy Theory of Value” and “Energy Return on Investment”—subjects of keen interest to peak-oil-aware students of economics. He also introduces “The Marginal Energy Return on Investment” as a measure of energy that makes sense to both physicists and economists. The author’s professional qualifications enable him to treat these subjects in a clear and original way.

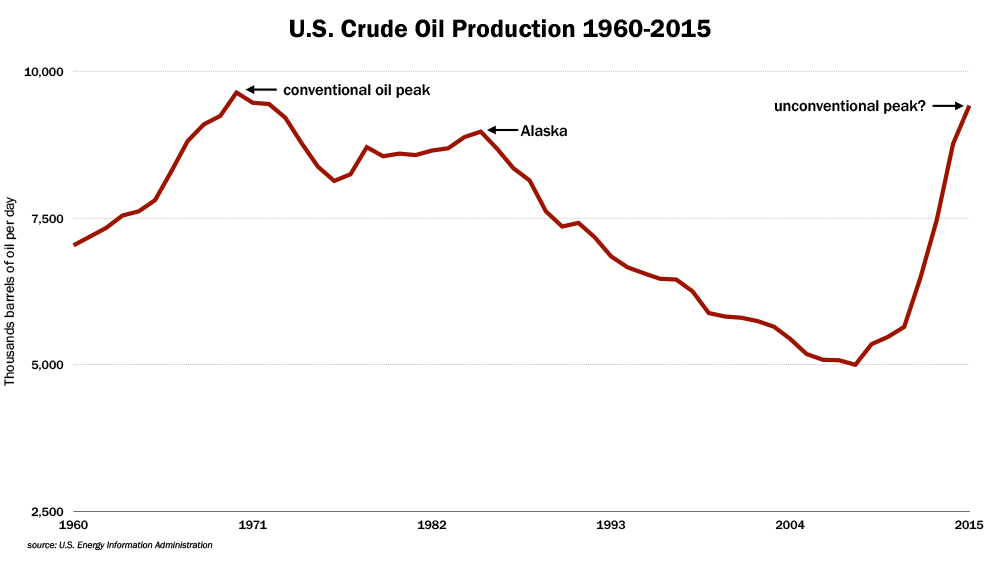

Then Reynolds addresses current world oil trends, including America’s oil production. The U.S. hit its all-time crude oil production high in 1970, but has seen two periods of post-peak output expansion—the first in the 1980s due to exploitation of Alaskan resources on the North Slope; the second in recent years as a result of applying hydrofracturing and horizontal drilling technologies to tight oil resources, mostly in North Dakota and Texas. The latter has given the world a reprieve from what would otherwise have been an earlier onset of total oil production decline, though it is as yet unclear how long the reprieve will last (see Exhibit A above).

Figure 3. U.S. Crude Oil Production, 1960-2015. Source: U.S. Energy Information Administration.

Readers familiar with the peak oil literature will remember that Dmitry Orlov covered some of these same themes in his book Reinventing Collapse: The Soviet Experience and American Prospects. However, Reynolds brings a very different set of skills and experiences to the discussion, and in drawing lessons from Soviet history comes to the following conclusions, some of which go beyond Orlov’s earlier work:

- Peak oil eventually comes.

- Oil consumption decline causes economic decline. Even a vibrant economy can succumb to peak oil.

- Oil is hard to substitute. Free markets can help with adaptation, but primarily on the demand side.

- Peak oil will cause peak government. There will be hyperinflation, and corruption will increase.

- A peak oil collapse can cause the disintegration of regional political ties. There will be new alliances.

- The military will decline.

Another new book, Failing States, Collapsing Systems: BioPhysical Triggers of Political Violence, by Nafeez Ahmed, covers overlapping subject matter. While peak oil is just one of the “biophysical triggers” of war, revolution, and terrorism that the author explores, Ahmed is one of the world’s best-informed journalists on energy supply issues.

Since the 2008 financial crash, social unrest has periodically erupted on every major continent—“from Greece to Ukraine, from China to Thailand, from Brazil to Turkey, and beyond.” Ahmed argues that policymakers and media observers have failed to comprehend the underlying causes of this tumult: the depletion of easily and cheaply accessed fossil fuels. The world’s increasing dependence on harder-to-get-at oil, in particular, has multiplying consequences for Earth’s climate, global food systems, and national economies, he claims.

Promotional materials for Ahmed’s book claim that it is the first to develop “an empirically grounded theoretical model of the complex interaction between biophysical processes and geopolitical crises, demonstrated through the analysis of a wide range of detailed case studies of historic, concurrent and probable state failures in the Middle East, Northwest Africa, South and Southeast Asia, Europe and North America.” While simplistic geopolitical theories are all too common, the best of them acknowledge the pivotal importance of essential resources.

In modern economies, the production and distribution of nearly all essential commodities (including food; see Figure 4) depends on energy in the forms of oil and electricity—most of which is typically generated from the burning of coal or natural gas. Thus energy systems, food systems, economic systems, and geopolitics are today inseparable, and a profound underlying shift in the quality and cost of our top energy source—i.e., petroleum—cannot help but have consequences that ripple through entire societies.

Figure 4. Caloric Inputs and Outputs per Capita in the United States, Based on Food Type (2002). Source; Canning, et al., Energy Use in the U.S. Food System, U.S. Department of Agriculture, 2010.

According to Ahmed, the depletion-led waning of the fossil fuel era is being accompanied by the compounding impacts of fossil fuel combustion, mostly in the form of climate change. The result is increasing disruptions in the availability of economic and ecological support services, even as more and more people require those services due to more frequent environmental disasters and continued population growth. This is a recipe for unstable governments, the rise of demagogues, the breakdown of alliances, and the emergence of new social movements. Nevertheless, the author holds out hope for a paradigmatic revolution in how civilization operates—“a fundamental epistemological shift recognizing humanity’s embeddedness in the natural world.”

Failing States, Collapsing Systems argues that international relations and domestic politics can only be understood by recognizing how “the political is embedded in the biophysical.” The book contains helpful graphical illustrations of oil production data, population, the food price index, economic growth, debt, and other relevant issues.

Implications for the Trump Administration

All of this underscores the realization that peak oil is potentially a very big deal (as many of us have been saying for a long time now). Again, the precise timing of the onset of the inevitable global petroleum production decline is still uncertain, though trends cited above suggest the oil world is getting increasingly “peaky”—both in terms of supply issues and signs of geopolitical flux. Also, the peak will in all likelihood not be marked as a sudden event, but instead will manifest itself via complex, protracted processes that include interactions among the oil industry, the economic system, the food system, and so on. Indeed, it’s highly likely that the vast majority of people will view the symptoms of the peak as the actual cause of the increasing stress they are experiencing—never recognizing the role that energy plays in the economy and the general functioning of society.

To this volatile mixture now add one Donald Trump. Serious and numerous questions immediately arise.

What will the Trump transition mean for energy? The president-elect appears to have some understanding of the importance of energy for the health of the economy, and he has promised to expand energy production. But how successful is he likely to be in this?

In a separate essay I have already addressed the impracticality of Trump’s goal of ramping up domestic coal mining. Suffice it to say, the coal industry is dying regardless what the new president does.

But what about oil and gas? The nomination of Rex Tillerson (CEO of ExxonMobil) as the next Secretary of State is a powerful clue. Matthieu Auzanneau, writing for Le Monde, notes that Tillerson is departing Exxon as the company drifts toward insolvency as a result of declining reserves, rising costs, and falling profits. Russia, the world’s top petro-state, faces the same problem. Could Tillerson, whose business liaisons with Russia are legendary, make oil exploration alliances a cornerstone of diplomacy? Meanwhile, Rick Perry, former Texas governor, who witnessed a huge drilling boom in his home state and a simultaneous expansion of wind power, has been picked to head the Department of Energy. And Oklahoma Attorney General Scott Pruitt, a climate denier and unfailingly loyal fossil fuel advocate, is slated to head the Environmental Protection Agency. Clearly, Trump is interested in facilitating more drilling, and in shifting the economic and regulatory frameworks that constrain it.

Removing or changing regulations could help to increase oil and gas production, but probably not by much. While exemptions to the Clean Water Act (pushed through by then-Vice President Dick Cheney in 2005) helped spur America’s fracking revolution, regulations are generally not the biggest factor in whether oil or gas production goes up or down; the main trigger is prices. Similarly, while the opening of more federal lands to drilling would constitute a gesture welcome to the oil and gas industry, it would not necessarily result in an imminent boost to production, since those lands hold few prospects that would entice the now heavily indebted industry to invest in risky exploration. A significant factor in the fracking boom was low interest rates; but interest rates are set by Federal Reserve policy, which the Trump administration cannot directly control.

How about renewable energy? Trump has made some unfriendly comments about solar and wind power, and may seek to reduce federal subsidies for renewables. While this attitude may flip (Trump’s views have been known to change dramatically and quickly; also recall Rick Perry’s support for wind power in Texas), even in the best-case scenario it is unlikely that we will see the dramatic shift toward renewables that would actually be needed in order to significantly mitigate climate change or help the nation adapt to the impacts of fossil fuel depletion. An enormous build-out of post-fossil fuel infrastructure is needed, and Trump has big infrastructure plans—but those plans amount to doubling down on the nation’s existing reliance on fossil fuels by building yet more highways, bridges, and airports. And the way he proposes to fund the expansion permits skepticism that much will actually get built in any case. (It’s worth noting, parenthetically, that Middle East sovereign wealth funds are pledging to invest in U.S. infrastructure—an investment that just might be geared at least in part toward keeping America hooked on fossil fuels.)

The advent of President Donald J. Trump clearly has implications for global geopolitics, but of what sort? Since the fall of the Soviet Union, U.S. geostrategists have embraced the goal of global hegemony, which meant preventing alliances between key Eurasian powers (Russia, China, Iran) and encircling them with U.S. military bases; maintaining a coherent group of prosperous allies (especially including Europe, Japan, and South Korea); using military force to ensure no noncompliant nation is left standing in the Middle East; and pursuing global wealth consolidation through dollar-denominated trade under the auspices of U.S.-led international treaties and institutions. In recent years this set of policies has been increasingly stymied by China’s dizzying economic ascent (which occurred with U.S. encouragement but is now posing a geopolitical liability); by Russia’s stabilization and recovery under a leader who resists U.S. control; by the spectacular failure of U.S. wars in the Middle East; by economic decline and political dissension within the European Union; and by increasing economic cooperation and security alignment among Russia, China, Iran, and other nations (including trade and banking arrangements that circumvent the dollar and U.S.-dominated global economic institutions like the IMF). Together, these developments seriously imperil the U.S. project of continued world supremacy. Indeed, the erosion of American power has reached a crucial tipping point where the goals and tactics of the incumbent geostrategists must be questioned, even by insiders.

Again, Trump arrives at a key moment, arguing against the demonization of Russia, promising to implement protectionist trade rules to bring manufacturing back to the U.S, and pledging no new wars in the Middle East. It is too early to speak of this tweet-list as constituting a coherent alternative geopolitical strategy. But Trump is already at odds with currently dominant elements within the CIA and the State Department (which, along with the Pentagon and military contractors, comprise the so-called Deep State), and is allying himself with previously sidelined voices. Formidable and secretive, the Deep State has a momentum of its own, which any national leader resists at his or her own peril.

The past few U.S. administrations have presided over a period of economic stagnation in which the illusion of continued growth was maintained by jiggered statistics, massive bailouts, a historic ballooning of public and private debt, and the financialization of the economy, with nearly all gains going to the one-percenters while most others fared worse and worse. Now the backstops to economic contraction are failing. Regardless whether Trump or Clinton prevailed in 2016, the next leader would face serious decay and instability across the spectrum of systems supporting the nation’s ongoing functions.

If this is indeed the timeframe when the global energy economy flips from fossil fuel-powered growth to depletion-led contraction, then the recent election presents us with a bewildering new landscape of circumstances in which that flip will occur, and an astonishing new set of actors. In a chilling paragraph, journalist Chris Hedges frames the moment in familiar terms:

“The final stages of capitalism, Karl Marx predicted, would be marked by global capital being unable to expand and generate profits at former levels. Capitalists would begin to consume the government along with the physical and social structures that sustained them. Democracy, social welfare, electoral participation, the common good and investment in public transportation, roads, bridges, utilities, industry, education, ecosystem protection and health care would be sacrificed to feed the mania for short-term profit. These assaults would destroy the host. This is the stage of late capitalism that Donald Trump represents.”

Hedges calls the new administration’s guiding impulse kleptocracy—rule by thieves. The signs of imminent kleptocracy are certainly abundant: proposed heads of governmental departments have promised to destroy regulations and privatize assets—all under the justification that doing so will lead to more growth and more jobs.

Given these radical shifts in priorities, expect a purge of government agencies. For those who pledge allegiance to Trump, there may be a secure salary in store. One doesn’t have to be particularly qualified or competent, just willing to turn in any co-worker heard grumbling about the exalted leader. Expect no work on climate change to go forward. The compilation of accurate statistics (on the environment, energy production, and the economy) may be largely abandoned. Companies eager to help with the program may be awarded generous government contracts; those that make a fuss may be penalized. States and cities that try to fight back against the new administration’s policies may be treated as sites of domestic rebellion. In the worst conceivable case, terrorist attacks could justify a massive national clampdown, in which uncompromising journalists and teachers might be targeted in the name of national unity.

The new administration will remain deeply resented by enormous swathes of the populace. A gutting of regulations might temporarily grease the skids of commerce, but at the cost of exposing vastly more people to fraud, pollution, preventable accidents, and poverty. This could eventually make a lot of folks very, very angry. If the new leadership uses ever more desperate means to consolidate and wield power, expect ever more extreme acts of resistance.

Anyone who claims to know in advance how all this will shake out is blowing smoke. This is the most combustible mix of circumstances I’ve seen in my lifetime. Donald Trump is certainly not the peak oil president I would have chosen. But he promises to be a pivotal historical figure.

For more on US energy prospects see Will the US Really Be a Major Energy Exporter?

A Good Day for a Walk in the Woods

(Written for inauguration day January 20th, 2016).

Not since the Civil War has an American presidential Inauguration Day been so fraught with fear and dread (on February 23, 1861, Abraham Lincoln traveled to his inauguration under military guard, arriving in Washington, D.C., in disguise). The incoming president is the most unpopular of any to assume office since modern polling began. In a single news cycle this past week he managed to alienate allies throughout an entire continent (Europe) during a brief break in a string of petulant tweets intended to persuade his own nation that Saturday Night Live is “not funny . . . really bad television!”

Much has been made of the new president’s personality and psyche—his narcissism, his germophobia, his irritability, his minimal sleeping habits, and his reported inability to laugh (though he does smile). In my view, the most revealing personal characteristic of president #45 may be his complete disconnection from the natural world. Here is an individual who grew up in a city, who sees land only in terms of profit potential, who proudly covers the tortured ground with high-rise buildings, who lives in a penthouse, and who walks outdoors only on golf courses. One could make some similar comments about many of his recent predecessors (certainly not Teddy Roosevelt), but in this instance the tendency reaches an extreme.

How can a person so isolated from natural phenomena hope to understand the vulnerability of our planet’s climate, water, air, and innumerable species to the actions of people (one hastens to add—people much like himself)? How can he appreciate that civilization itself is an organism with a constant need for “food” (not just grain and meat, but energy, minerals, and water as well), that is organized by way of hierarchically ordered and interlinked cycles, and that is subject to natural limits and ultimately to death?

One could argue that all hubris is tied to human beings’ illusion of dominance over nature. Our long withdrawal from wildness surely started with language, which gave us the ability to name and categorize, and thus to psychically control and distance ourselves from what we named; it erupted into alienation with the advent of agriculture, cities, and most recently fossil fuels. But we never stopped depending on the fabric of life in which we have always been entwined. Even as we unravel the ecosphere’s delicate fibers, we draw upon eons of accumulated soil nutrients and minerals, fresh water, and biodiversity.

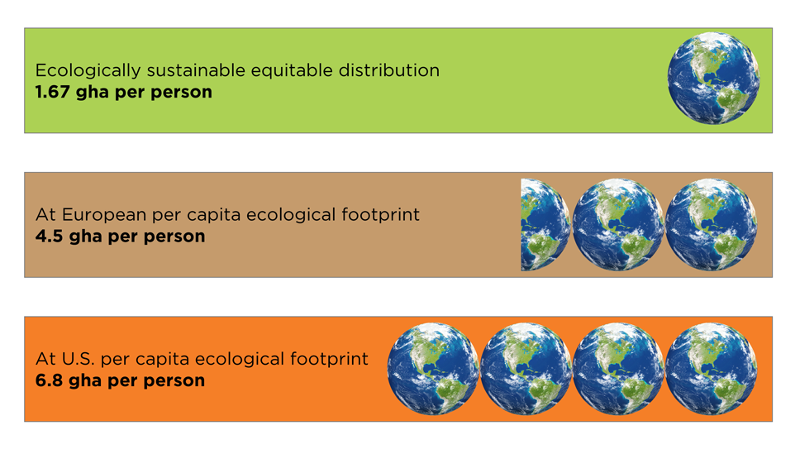

Life implies death—one’s own mortality above all. Everything has limits. Wisdom resides in the understanding that we are subject to forces we cannot control, and that we must respect and accommodate ourselves to those forces. If we want to have language, farming, cities, and energy, then we must make a deliberate cultural effort to maintain an attitude of individual and collective humility. In practical terms, that means keeping the size of our global population low enough so that it can be supported long-term without eroding natural systems, managing consumption so that resources are not depleted and non-biodegradable wastes do not accumulate, and maintaining checks on wealth inequality.

Figure: How many Earths does it take? Productive global hectares (gha) per capita required for the current world population. Data source: Global Footprint Network.

Obviously, we haven’t been doing these things very well, especially in recent decades. The power of fossil fuels fed our collective megalomania. Like people in previous civilizations, we went out on a limb—but modern energy and technology enabled us to go much further than any humans had before. Still, as all civilizations do, ours has reached the point of diminishing returns, of over-reach. Before us lies the senescence and death of a way of living and of seeing the world. Perhaps the new president’s qualities of character are emblematic of these final stages of cultural disintegration.

In the days to come, there will be plenty of opportunities for resistance, protest, and, one hopes, celebration. Inauguration Day 2017 is a turning point; for me, it seems a perfect occasion for a walk in the woods.

Trump photo credit: Evan El-Amin/Shutterstock.com