![[Power book cover]](https://richardheinberg.com/wp-content/uploads/2021/03/cover_POWERcatalog-proof_300x450.jpg)

MuseLetter #356 / November 2022 by Richard Heinberg

Download printable PDF version

This month’s Museletter begins with a tribute to Herman Daly, the father of ecological economics. Also included are the first two parts of a trilogy written for Independent Media Institute on the renewable energy transition.

The Final Doubling

This essay is dedicated to the memory of Herman Daly, the father of ecological economics, who began writing about the absurdity of perpetual economic growth in the 1970s; Herman died on October 28 at age 84.

Politicians and economists talk glowingly about growth. They want our cities and GDP to grow. Jobs, profits, companies, and industries all should grow; if they don’t, there’s something wrong, and we must identify the problem and fix it. Yet few discuss doubling time, even though it’s an essential concept for understanding growth.

Doubling time helps us grasp the physical meaning of growth—which otherwise appears as an innocuous-looking number denoting the annual rate of change. At 1 percent annual growth, any given quantity doubles in about 70 years; at 2 percent growth, in 35 years; at 7 percent, in 10 years, and so on. Just divide 70 by the annual growth rate and you’ll get a good sense of doubling time. (Why 70? It’s approximately the natural logarithm of 2. But you don’t need to know higher math to do useful doubling-time calculations.)

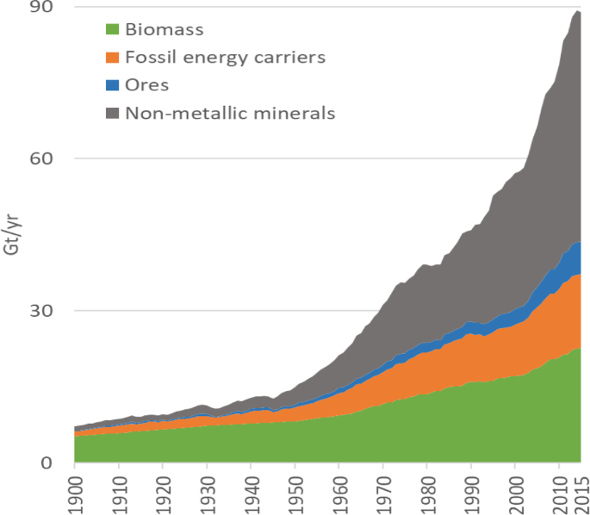

Here’s why failure to think in terms of doubling time gets us into trouble. Most economists seem to believe that a 2 to 3 percent annual rate of growth for economies is healthy and normal. But that implies a doubling time of roughly 25 years. When an economy grows, it uses more physical materials—everything from trees to titanium. Indeed, the global economy has doubled in size in the last quarter-century, and so has total worldwide extraction of materials. Since 1997 we have used over half the non-renewable resources extracted since the origin of humans.

As the economy grows, it also puts out more waste. In the last 25 years, the amount of solid waste produced globally has soared from roughly 3 million tons per day to about 6 million tons per day.

Global materials extraction and usage, 1900 to 2015. Source: Arnulf Grubler, Technological and Societal Changes and Their Impacts on Resource Production and Use.

NOTE: higher res version here

Further, if the economy keeps growing at the recent rate, in the next 25 years we will approximately double the amount of energy and materials we use. And by 50 years from today our energy and materials usage will have doubled again, and will therefore be four times current levels. In a hundred years, we will be using 16 times as much. If this same 2 to 3 percent rate of growth were to persist for a century beyond that, by the year 2222 we’d be using about 250 times the amount of physical resources we do now, and we’d be generating about 250 times as much waste.

Population growth can also be described in terms of doublings. Global human population has doubled three times in the past 200 years, surging from 1 billion in 1820 to 2 billion in 1927, to 4 billion in 1974, to 8 billion today. Its highest rate of growth was in the 1960s, at over 2 percent per year; that rate is now down to 1.1 percent. If growth continues at the current rate, we’ll have about 18 billion people on Earth by the end of this century.

All of this would be fine if we lived on a planet that was itself expanding, doubling its available quantities of minerals, forests, fisheries, and soil every quarter-century, and doubling its ability to absorb industrial wastes. But we don’t. It is essentially the same beautiful but finite planet that was spinning through space long before the origin of humans.

Young people might think of 25 years as a long time. But, given the centuries it takes to regrow a mature forest, or the millennia it takes to produce a few inches of topsoil, or the tens of millions of years it took nature to produce fossil fuels, 25 years is a comparative eyeblink. And in that eyeblink, humanity’s already huge impact on Earth’s finely balanced ecosystems doubles.

Since resources are finite, the doubling of humanity’s rates of extracting them can’t go on forever. Economists try to get around this problem by hypothesizing that economic growth can eventually be decoupled from greater usage of resources. Somehow, according to the hypothesis, GDP (essentially a measure of the amount of money flowing through the economy) will continue to climb, but we’ll spend our additional money on intangible goods instead of products made from physical stuff. So far, however, the evidence shows that decoupling hasn’t occurred in the past and is unlikely to happen in the future. Even cryptocurrencies, seemingly the most ephemeral of goods, turn out to have a huge material footprint.

As long as we continue to pursue growth, we are on track to attempt more doublings of resource extraction and waste dumping. But, at some point, we will come up short. When that final doubling fails, a host of expectations will be dashed. Investment funds will go broke, debt defaults will skyrocket, businesses will declare bankruptcy, jobs will disappear, and politicians will grow hoarse blaming one another for failure to keep the economy expanding. In the worst-case scenario, billions of people could starve and nations could go to war over whatever resources are left.

Nobody wants that to happen. So, of course, it would help to know when the last doubling will begin, so we can adjust our expectations accordingly. Do we have a century or two to think about all of this? Or has the final, ill-fated doubling already started?

Forecasting the Start of the Final Doubling—It’s Hard!

One of the problems with exponential acceleration of consumption is that the warning signs of impending resource scarcity tend to appear very close to the time of actual scarcity. During the final doubling, humanity will be using resources at the highest rates in history—so it will likely seem to most people that everything is going swimmingly, just when the entire human enterprise is being swept toward a waterfall.

Trying to figure out exactly when we’ll go over the falls is hard also because resource estimates are squishy. Take a single mineral resource—copper ore. The US Geological Survey estimates global copper reserves at 870 million metric tons, while annual copper demand is 28 million tons. So, dividing the first number by the second, it’s clear that we have 31 years’ worth of copper left at current rates of extraction. But nobody expects the global rate of copper mining to stay the same for the next 31 years. If the rate of extraction were to grow at 2.5 percent per year, then current reserves would be gone in a mere 22 years.

But that’s a simplistic analysis. Lower grades of copper ore, which are not currently regarded as commercially viable, are plentiful; with added effort and expense those resources could be extracted and processed. Further, there is surely more copper left to be discovered. A key bit of evidence in this regard is the fact that copper reserves have grown in some years, rather than diminishing. (On the other hand, the World Economic Forum has pointed out that the average cost of producing copper has risen by over 300 percent in recent years, while average copper ore grade has dropped by 30 percent.)

What if we were to recycle all the copper we use? Well, we should certainly try. But, disregarding any practical impediments, there’s the harsh reality that, as long as usage rates are growing, we’ll still need new sources of the metal, and the rate at which we’re depleting reserves will increase.

If all else fails, there are other metals that can serve as substitutes for copper. However, those other metals are also subject to depletion, and some of them won’t work as well as copper for specific applications.

Altogether, the situation is complicated enough that a reliable date for “peak copper,” or for when copper shortages will cause serious economic pain, is hard to estimate. This uncertainty, generalized to apply to all natural resources, leads some resource optimists to erroneously conclude that humanity will never face resource scarcity.

Here’s the thing though: if extraction is growing at 3 percent annually for a given resource, any underestimate won’t be off by very many years. That’s due to the power of exponentially growing extraction. For example, let’s say an analyst underestimates unobtanium reserves by half. In other words, there’s twice as much unobtanium in the ground as the analyst predicted. The date of the last bit of unobtanium extraction will only be 25 years later than what was forecast. Underestimating the abundance of a resource by three-quarters implies a run-out date that’s only 50 years too soon.

We’re In It

Resource depletion isn’t the only limit to the continued growth of the human enterprise. Climate change is another threat capable of stopping civilization in its tracks.

Our planet is warming as a result of greenhouse gas emissions—pollutants produced mainly by our energy system. Fossil fuels, the basis of that system, are cheap sources of densely stored energy that have revolutionized society. It’s because of fossil fuels that industrial economies have grown so fast in recent decades. In addition to causing climate change, fossil fuels are also subject to depletion: oilfields and coalmines are typically exhausted in a matter of decades. So, virtually nobody expects that societies will still be powering themselves with coal, oil, or natural gas a century from now; indeed, some experts anticipate fuel supply problems within years.

The main solution to climate change is for society to switch energy sources—to abandon fossil fuels as quickly as possible and replace them with solar and wind power. However, these alternative energy sources require infrastructure (panels, turbines, batteries, expanded grids, and new electrically powered machinery such as electric cars and trucks) that must be constructed using minerals and metals, many of which are rare. Some resource experts doubt that there are sufficient minerals to build an alternative energy system on a scale big enough to replace our current fossil-fueled energy system. Simon Michaux of the Finnish Geological Survey declares flatly that, “Global reserves are not large enough to supply enough metals to build the renewable non-fossil fuels industrial system.” Even if Michaux’s resource estimates are too pessimistic, it is still probably unrealistic to imagine that a renewables-based energy system will be capable of doubling in size even once, much less every 25 years forever more.

So, if another doubling of the global economy is impossible, that means the last doubling is already under way, and perhaps even nearing its conclusion.

It is better to anticipate the final doubling too soon rather than too late, because it will take time to shift expectations away from continuous growth. We’ll have to rethink finance and government planning, rewrite contracts, and perhaps even challenge some of the basic precepts of capitalism. Such a shift might easily require 25 years. Therefore, we should begin—or already should have begun—preparing for the end of growth at the start of the final doubling, at a time when it still appears to many people that energy and resources are abundant.

Re-localize, reduce, repair, and reuse. Build resilience. Become more independent of the monetary economy in any neighborly ways you can.

The next two articles were produced by Earth | Food | Life, a project of the Independent Media Institute.

Is the Energy Transition Taking Off—or Hitting a Wall?

With the Inflation Reduction Act, the federal government is illogically encouraging the increasing use of fossil fuels—in order to reduce our reliance on fossil fuels.

The passage of the Inflation Reduction Act (IRA) constitutes the boldest climate action so far by the American federal government. It offers tax rebates to buyers of electric cars, solar panels, heat pumps, and other renewable-energy and energy-efficiency equipment. It encourages the development of carbon-capture technology and promotes environmental justice by cleaning up pollution and providing renewable energy in disadvantaged communities. Does this political achievement mean that the energy transition, in the U.S. if not the world as a whole, is finally on track to achieving the goal of net zero emissions by 2050?

If only it were so.

Emissions modelers have estimated that the IRA will reduce U.S. emissions by 40 percent by 2030. But, as Benjamin Storrow at Scientific American has pointed out, the modelers fail to take real-world constraints into account. For one thing, building out massive new renewable energy infrastructure will require new long-distance transmission lines, and entirely foreseeable problems with permitting, materials, and local politics cast doubt on whether those lines can be built.

But perhaps the most frustrating barriers to grid modernization are the political ones. While Texas produces a significant amount of wind and solar electricity, it is unable to share that bounty with neighboring states because it has a stand-alone grid. And that’s unlikely to change because Texas politicians fear that connecting their grid with a larger region would open the state’s electricity system to federal regulation. Similar state-based regulatory heel-dragging is pervasive elsewhere. In a report posted in July, the North Carolina Clean Energy Technology Center noted that, so far this year, Texas regulators have approved only $478.7 million out of the $12.86 billion (3.7 percent) in grid modernization investment under consideration, due to fears of raising utility bills for local residents.

But grid modernization is only one area in which the energy transition is confronting roadblocks in the U.S.

Certainly, as a result of the IRA, more electric vehicles (EVs) will be purchased. California’s recent ruling to phase out new gas-powered cars by 2035 will buttress that trend. Currently, just under 5 percent of cars sold in the U.S. are EVs. By 2030, some projections suggest the proportion will be half, and by 2050 the great majority of light-duty vehicles on the road should be electric. However, those estimates assume that enough vehicles can be manufactured: Supply-chain issues for electronics and for battery materials have slowed deliveries of EVs in recent months, and those issues could worsen. Further, the IRA electric-vehicle tax credits will go only to buyers of cars whose materials are sourced in the U.S. That’s probably good in the long run, as it will reduce reliance on long supply chains for materials. But it raises questions about localized environmental and human impacts of increased mining.

Many environmentalists are thrilled with the IRA; others less so. Those in the more critical camp have pointed disapprovingly to the bill’s promotion of nuclear, and note that, in order to gain Senator Joe Manchin’s vote, Democrats agreed to streamline oil and gas pipeline approvals in a separate bill. In effect, the government will be encouraging the increasing use of fossil fuels … in order to reduce our reliance on fossil fuels.

Despite the flaws of the Inflation Reduction Act, it is likely the best that the federal government can accomplish in terms of climate progress for the foreseeable future. This is a country mired in institutional gridlock, its politics trapped in endless culture wars, with a durable Supreme Court majority intent on hampering the government’s ability to regulate carbon emissions.

Climate leadership is needed in the U.S., the country responsible for the largest share of historic emissions and is the second-biggest emitter (on a per-capita basis, the U.S. ranks far ahead of China, the top emitter). Without the U.S., global progress in reducing greenhouse gas emissions will be difficult. But the American political system, pivotal as it is in the project, is only the tip of the proverbial iceberg of problems with the shift from fossil fuels to renewables. The barriers to meeting climate goals are global and pervasive.

Global Inertia and Roadblocks

Consider Germany, which has been working on energy transition longer and harder than any other large industrial nation. Now, as Russia is withholding natural gas supplies following its invasion of Ukraine and NATO’s hostile reaction, German electricity supplies are tight and about to get tighter. In response, Germany’s Green Party is leading the push to restart coal power plants rather than halting the planned shuttering of nuclear power plants. And it’s splitting environmentalists. Further, the country’s electricity problems have been exacerbated by a lack of, well, wind.

Unless Russia increases natural gas supplies headed west, European manufacturing could largely shut down this winter—including the manufacturing of renewable energy and related technologies. UK day-ahead wholesale electricity prices have hit ten times the last decade’s average price, and Europe faces energy scarcity this winter. French President Emmanuel Macron recently warned that his people face the “end of abundance.”

Inadequate spending is also inhibiting a renewables takeoff. Last year, EU member states spent over $150 billion on the energy transition, compared to about $120 billion by the U.S. Meanwhile, China spent nearly $300 billion on renewable energy and related technologies. According to the China Renewable Energy Engineering Institute, the country will install 156 gigawatts of wind turbines and solar panels this year. In comparison, the U.S., under the Inflation Reduction Act, would grow renewable energy annual additions from the current rate of about 25 GW per year to roughly 90 GW per year by 2025, with growth rates increasing thereafter, according to an analysis by researchers at Princeton University.

The recent remarkable increase in spending is far from sufficient. Last year, the world spent a total of about $530 billion on the energy transition (for comparison’s sake, the world spent $700 billion on fossil fuel subsidies in 2021). However, to bring worldwide energy-related carbon dioxide emissions to be net zero by 2050, annual capital investment in the transition would need to grow by over 900 percent, reaching nearly $5 trillion by 2030, according to the International Energy Agency. Bloomberg writer Aaron Clark notes,

“The one thing public climate spending plans in the U.S., China, and the EU all have in common is that the investments aren’t enough.”

There’s one other hurdle to addressing climate change that goes almost entirely unnoticed. Most cost estimates for the transition are in terms of money. What about the energy costs? It will take a tremendous amount of energy to mine materials; transport and transform them through industrial processes like smelting; turn them into solar panels, wind turbines, batteries, vehicles, infrastructure, and industrial machinery; install all of the above, and do this at a sufficient scale to replace our current fossil-fuel-based industrial system. In the early stages of the process, this energy will have to come mostly from fossil fuels, since they supply about 83 percent of current global energy. The result will surely be a pulse of emissions; however, as far as I know, nobody has tried to calculate its magnitude.

The requirement to reduce our reliance on fossil fuels represents the biggest technical challenge humanity has ever faced. To avoid the emissions pulse just mentioned, we must reduce energy usage in non-essential applications (such as for tourism or the manufacture of optional consumer goods). But such reductions will provoke social and political pushback, given that economies are structured to require continual growth, and citizens are conditioned to expect ever-higher levels of consumption. If the energy transition is the biggest technical challenge ever, it is also the biggest social, economic, and political challenge in human history. It may also turn out to be an enormous geopolitical challenge, if nations end up fighting over access to the minerals and metals that will be the enablers of the energy transition.

The Renewable Energy Transition Is Failing

Renewable energy isn’t replacing fossil fuel energy—it’s adding to it.

Despite all the renewable energy investments and installations, actual global greenhouse gas emissions keep increasing. That’s largely due to economic growth: While renewable energy supplies have expanded in recent years, world energy usage has ballooned even more—with the difference being supplied by fossil fuels. The more the world economy grows, the harder it is for additions of renewable energy to turn the tide by actually replacing energy from fossil fuels, rather than just adding to it.

The notion of voluntarily reining in economic growth in order to minimize climate change and make it easier to replace fossil fuels is political anathema not just in the rich countries, whose people have gotten used to consuming at extraordinarily high rates, but even more so in poorer countries, which have been promised the opportunity to “develop.”

After all, it is the rich countries that have been responsible for the great majority of past emissions (which are driving climate change presently); indeed, these countries got rich largely by the industrial activity of which carbon emissions were a byproduct. Now it is the world’s poorest nations that are experiencing the brunt of the impacts of climate change caused by the world’s richest. It’s neither sustainable nor just to perpetuate the exploitation of land, resources, and labor in the less industrialized countries, as well as historically exploited communities in the rich countries, to maintain both the lifestyles and expectations of further growth of the wealthy minority.

From the perspective of people in less-industrialized nations, it’s natural to want to consume more, which only seems fair. But that translates to more global economic growth, and a harder time replacing fossil fuels with renewables globally. China is the exemplar of this conundrum: Over the past three decades, the world’s most populous nation lifted hundreds of millions of its people out of poverty, but in the process became the world’s biggest producer and consumer of coal.

The Materials Dilemma

Also posing an enormous difficulty for a societal switch from fossil fuels to renewable energy sources is our increasing need for minerals and metals. The World Bank, the IEA, the IMF, and McKinsey and Company have all issued reports in the last couple of years warning of this growing problem. Vast quantities of minerals and metals will be required not just for making solar panels and wind turbines, but also for batteries, electric vehicles, and new industrial equipment that runs on electricity rather than carbon-based fuels.

Some of these materials are already showing signs of increasing scarcity: According to the World Economic Forum, the average cost of producing copper has risen by over 300 percent in recent years, while copper ore grade has dropped by 30 percent.

Optimistic assessments of the materials challenge suggest there are enough global reserves for a one-time build-out of all the new devices and infrastructure needed (assuming some substitutions, with, for example, lithium for batteries eventually being replaced by more abundant elements like iron). But what is society to do as that first generation of devices and infrastructure ages and requires replacement?

Circular Economy: A Mirage?

Hence the rather sudden and widespread interest in the creation of a circular economy in which everything is recycled endlessly. Unfortunately, as economist Nicholas Georgescu-Roegen discovered in his pioneering work on entropy, recycling is always incomplete and always costs energy. Materials typically degrade during each cycle of use, and some material is wasted in the recycling process.

A French preliminary analysis of the energy transition that assumed maximum possible recycling found that a materials supply crisis could be delayed by up to three centuries. But will the circular economy (itself an enormous undertaking and a distant goal) arrive in time to buy industrial civilization those extra 300 years? Or will we run out of critical materials in just the next few decades in our frantic effort to build as many renewable energy devices as we can in as short a time as possible?

The latter outcome seems more likely if pessimistic resource estimates turn out to be accurate. Simon Michaux of the Finnish Geological Survey finds that “[g]lobal reserves are not large enough to supply enough metals to build the renewable non-fossil fuels industrial system … Mineral deposit discovery has been declining for many metals. The grade of processed ore for many of the industrial metals has been decreasing over time, resulting in declining mineral processing yield. This has the implication of the increase in mining energy consumption per unit of metal.”

Steel prices are already trending higher, and lithium supplies may prove to be a bottleneck to rapidly increasing battery production. Even sand is getting scarce: Only certain grades of the stuff are useful in making concrete (which anchors wind turbines) or silicon (which is essential for solar panels). More sand is consumed yearly than any other material besides water, and some climate scientists have identified it as a key sustainability challenge this century. Predictably, as deposits are depleted, sand is becoming more of a geopolitical flashpoint, with China recently embargoing sand shipments to Taiwan with the intention of crippling Taiwan’s ability to manufacture semiconductor devices such as cell phones.

To Reduce Risk, Reduce Scale

During the fossil fuel era, the global economy depended on ever-increasing rates of extracting and burning coal, oil, and natural gas. The renewables era (if it indeed comes into being) will be founded upon the large-scale extraction of minerals and metals for panels, turbines, batteries, and other infrastructure, which will require periodic replacement.

These two economic eras imply different risks: The fossil fuel regime risked depletion and pollution (notably atmospheric carbon pollution leading to climate change); the renewables regime will likewise risk depletion (from mining minerals and metals) and pollution (from dumping old panels, turbines, and batteries, and from various manufacturing processes), but with diminished vulnerability to climate change. The only way to lessen risk altogether would be to reduce substantially society’s scale of energy and materials usage—but very few policymakers or climate advocacy organizations are exploring that possibility.

Climate Change Hobbles Efforts to Combat Climate Change

As daunting as they are, the financial, political, and material challenges to the energy transition don’t exhaust the list of potential barriers. Climate change itself is also hampering the energy transition—which, of course, is being undertaken to avert climate change.

During the summer of 2022, China experienced its most intense heat wave in six decades. It impacted a wide region, from central Sichuan Province to coastal Jiangsu, with temperatures often topping 40 degrees Celsius, or 104 degrees Fahrenheit, and reaching a record 113 degrees in Chongqing on August 18. At the same time, a drought-induced power crisis forced Contemporary Amperex Technology Co., the world’s top battery maker, to close manufacturing plants in China’s Sichuan province. Supplies of crucial parts to Tesla and Toyota were temporarily cut off.

Meanwhile, a similarly grim story unfolded in Germany, as a record drought reduced the water flow in the Rhine River to levels that crippled European trade, halting shipments of diesel and coal, and threatening the operations of both hydroelectric and nuclear power plants.

A study published in February 2022 in the journal Water found that droughts (which are becoming more frequent and severe with climate change) could create challenges for U.S. hydropower in Montana, Nevada, Texas, Arizona, California, Arkansas, and Oklahoma.

Meanwhile, French nuclear plants that rely on the Rhône River for cooling water have had to shut down repeatedly. If reactors expel water downstream that’s too hot, aquatic life is wiped out as a result. So, during the sweltering 2022 summer, Électricité de France (EDF) powered down reactors not only along the Rhône but also on a second major river in the south, the Garonne. Altogether, France’s nuclear power output has been cut by nearly 50 percent during the summer of 2022. Similar drought- and heat-related shutdowns happened in 2018 and 2019.

Heavy rain and flooding can also pose risks for both hydro and nuclear power—which together currently provide roughly four times as much low-carbon electricity globally as wind and solar combined. In March 2019, severe flooding in southern and western Africa, following Cyclone Idai, damaged two major hydro plants in Malawi, cutting off power to parts of the country for several days.

Wind turbines and solar panels also rely on the weather and are therefore also vulnerable to extremes. Cold, cloudy days with virtually no wind spell trouble for regions heavily reliant on renewable energy. Freak storms can damage solar panels, and high temperatures reduce panels’ efficiency. Hurricanes and storm surges can cripple offshore wind farms.

The transition from fossil fuel to renewables faces an uphill battle. Still, this switch is an essential stopgap strategy to keep electricity grids up and running, at least on a minimal scale, as civilization inevitably turns away from a depleting store of oil and gas. The world has become so dependent on grid power for communications, finance, and the preservation of technical, scientific, and cultural knowledge that, if the grids were to go down permanently and soon, it is likely that billions of people would die, and the survivors would be culturally destitute. In essence, we need renewables for a controlled soft landing. But the harsh reality is that, for now, and in the foreseeable future, the energy transition is not going well and has poor overall prospects.

We need a realistic plan for energy descent, instead of foolish dreams of eternal consumer abundance by means other than fossil fuels. Currently, politically rooted insistence on continued economic growth is discouraging truth-telling and serious planning for how to live well with less.

Teaser photo credit: A mining farm of Genesis Mining located in Iceland. The picture shows mainly Zeus scrypt miners. By Marco Krohn, Wikimedia – Own work, CC BY-SA 4.0